|

|

| Making learning and work count Labour market LIVE from Learning and Work Institute 23 March 2021

One year on: Labour market impacts of coronavirus and priorities for the years ahead This morning, we have published our new ‘One year on’ report. This shows the labour market impact of coronavirus over the last year, its unequal impacts, and priorities for the years ahead to increase employment, reduce inequalities and support incomes. Learning and Work Institute comment

Overall, the safest conclusion is that the labour market is, as The Raconteurs might say in ‘Steady as she goes’ mode. A period of turbulence is starting to be followed by something that is beginning to look more stable. While this is positive news, it is also clear that the pandemic will continue to have adverse consequences for years to come. Long-term unemployment (12 months plus) has risen by more than a third (37 percent) in the last six months. Even more worryingly, youth long-term unemployment (6 months plus) has risen by almost two-thirds (64 percent) over the same period. There is a significant body of research showing that youth unemployment can have very long lasting adverse scarring effects on individuals’ subsequent chances of being in work and, on their wage levels when in work with some studies showing wage impacts lasting for more than twenty years. Employees who have remained formally employed but furloughed who have not worked for an extended period and who subsequently lose their jobs may also struggle to return to work in similar ways to the long term

unemployed. Paul Bivand, Assistant Director for Statistics and Analysis at Learning and Work Institute said: |

|

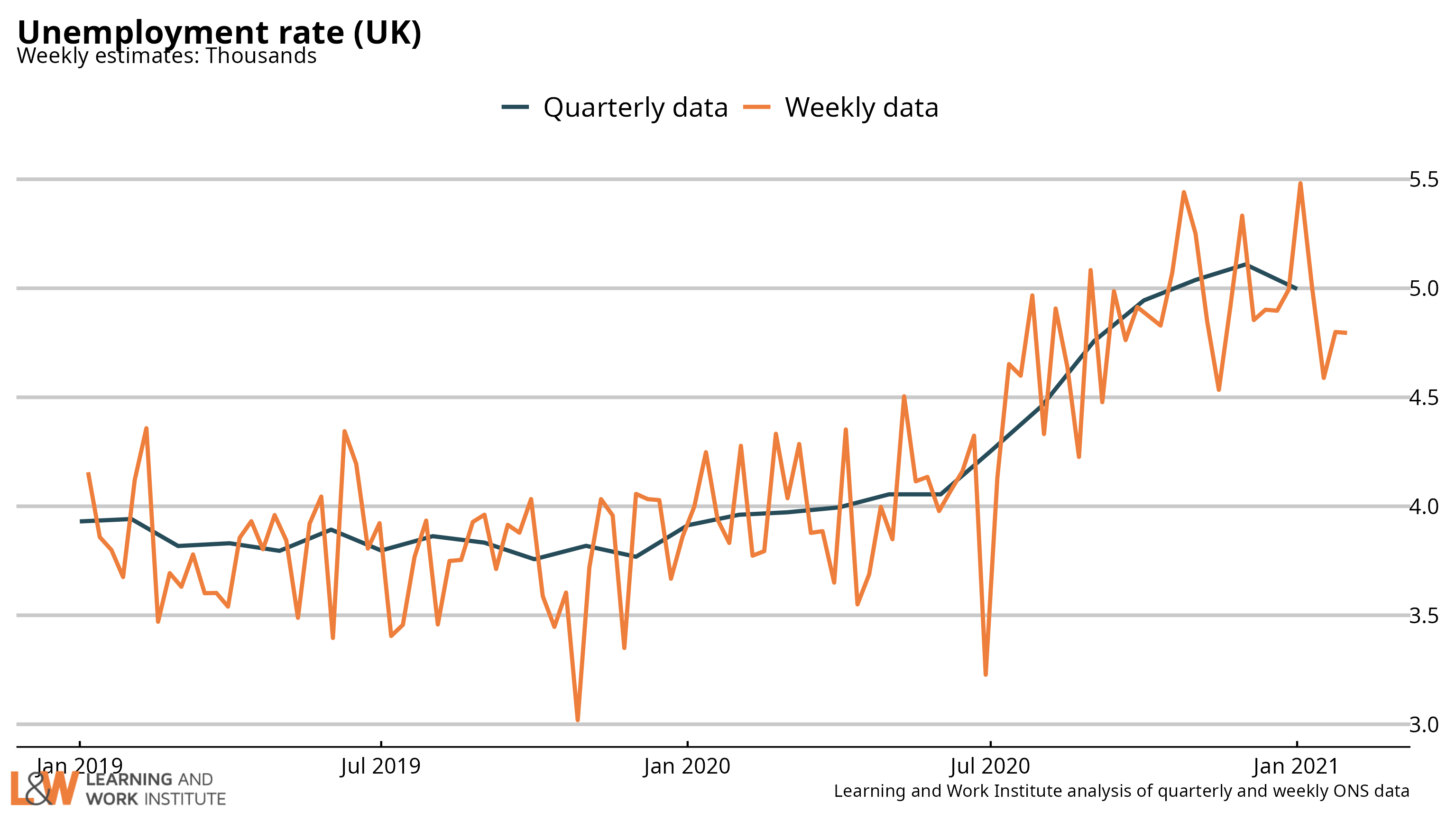

| Chart 1: UK unemployment (ILO) The latest unemployment rate fell by 0.1 percentage points to 5.0%.  |

|

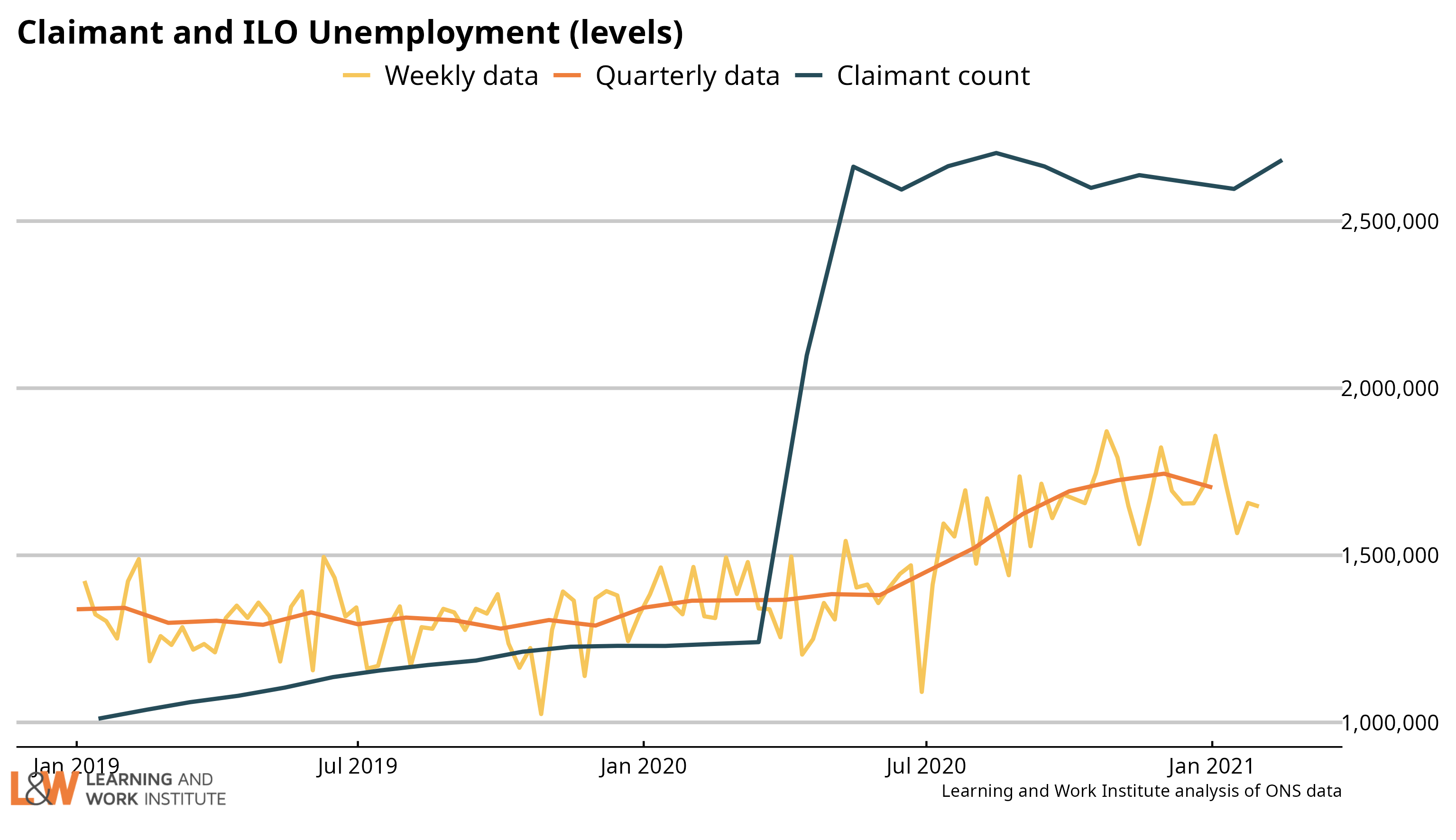

| Chart 2: The claimant count and UK unemployment compared The number of unemployed people who are claiming unemployment-related benefits is now 980,000 higher than the number of unemployed in the official measure.  |

|

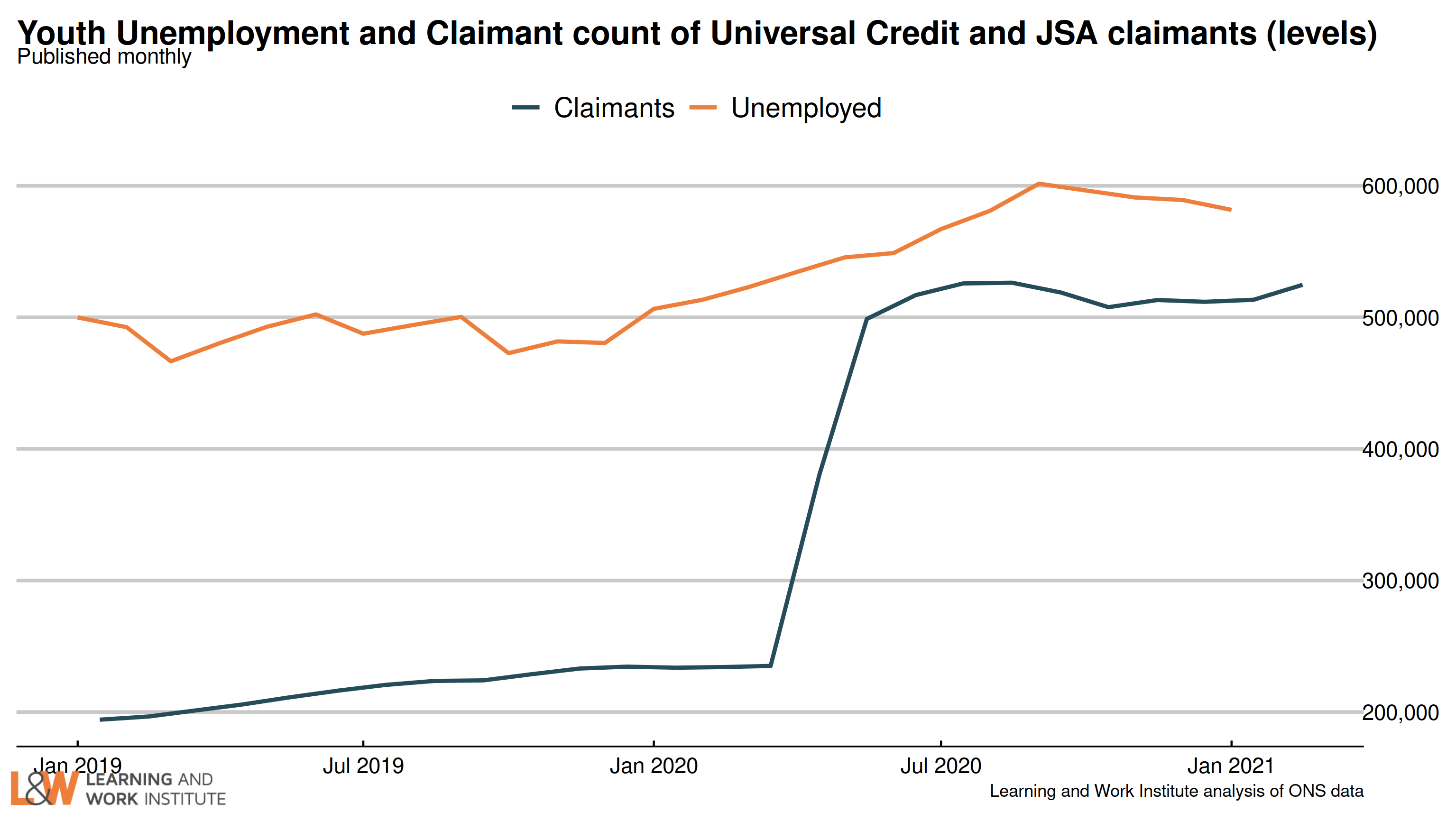

| Chart 3: Youth unemployment The number of unemployed young people is down by 8,000 since last month’s figures, to 582,000. Meanwhile, the number of young Universal Credit or Jobseeker’s Allowance claimants increased last month by 11,400, to 524,800.  |

|

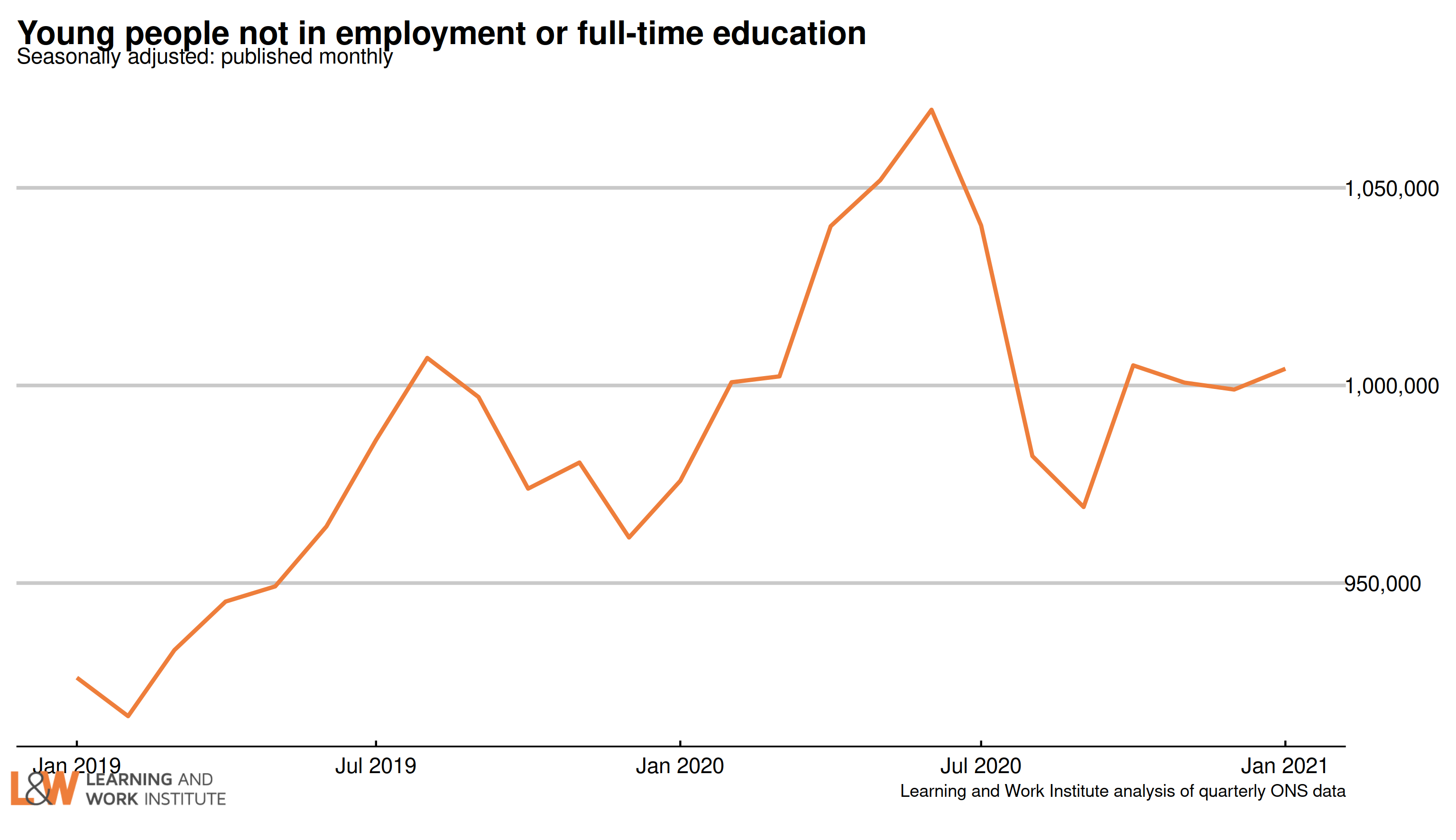

| Chart 4: Young people not in employment, full-time education or training The number of out of work young people who are not in full-time education (1,004,000) reduced by 1,000 in the last quarter , or 0.1%.  |

|

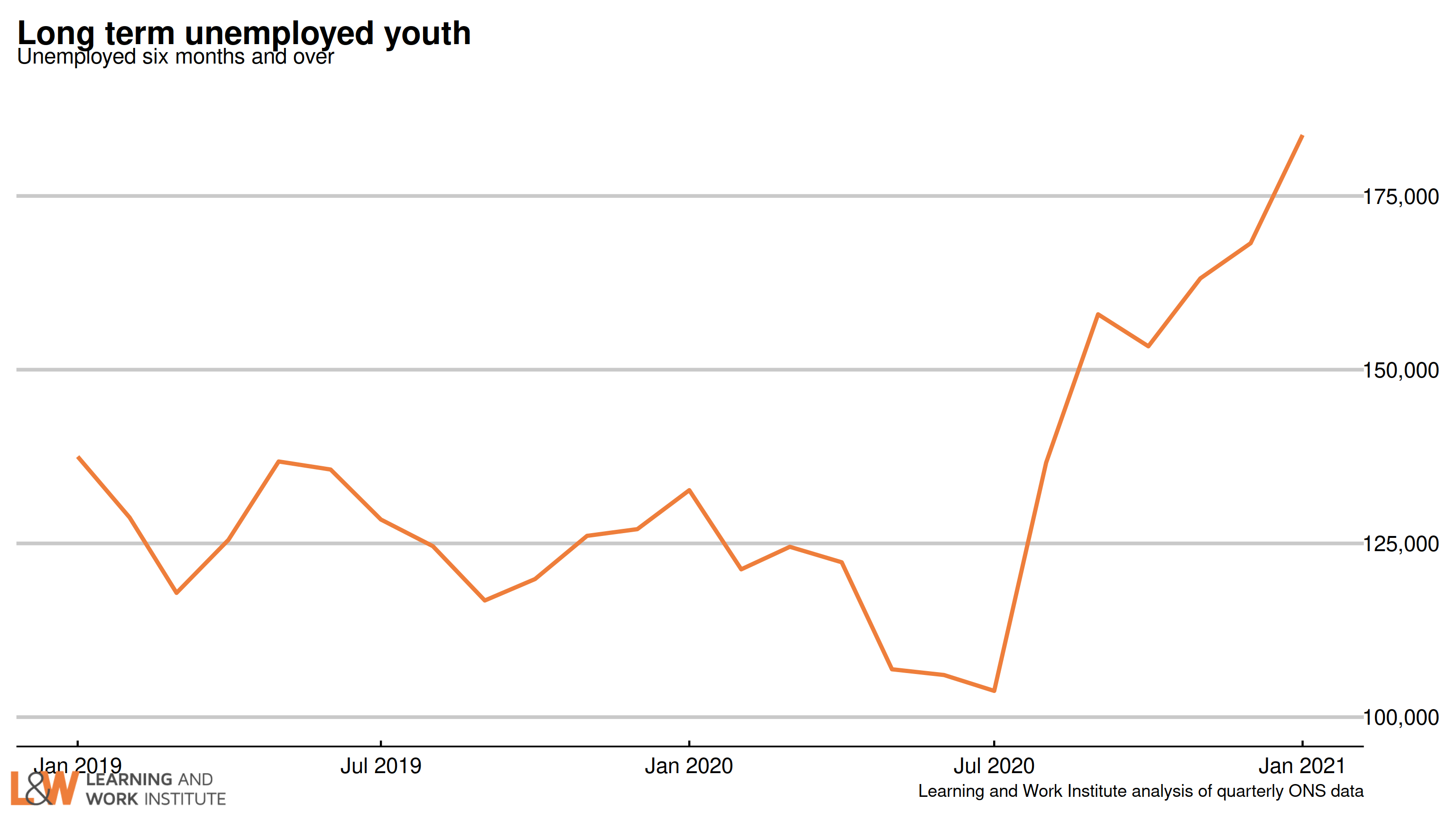

| Chart 5: Youth long-term unemployment (six months and over, 18-24) Youth long-term unemployment (which can include students) has risen by 30,000 over the last quarter and is now 184,000. This is up 20% on the previous quarter, and 39% on a year before.  |

|

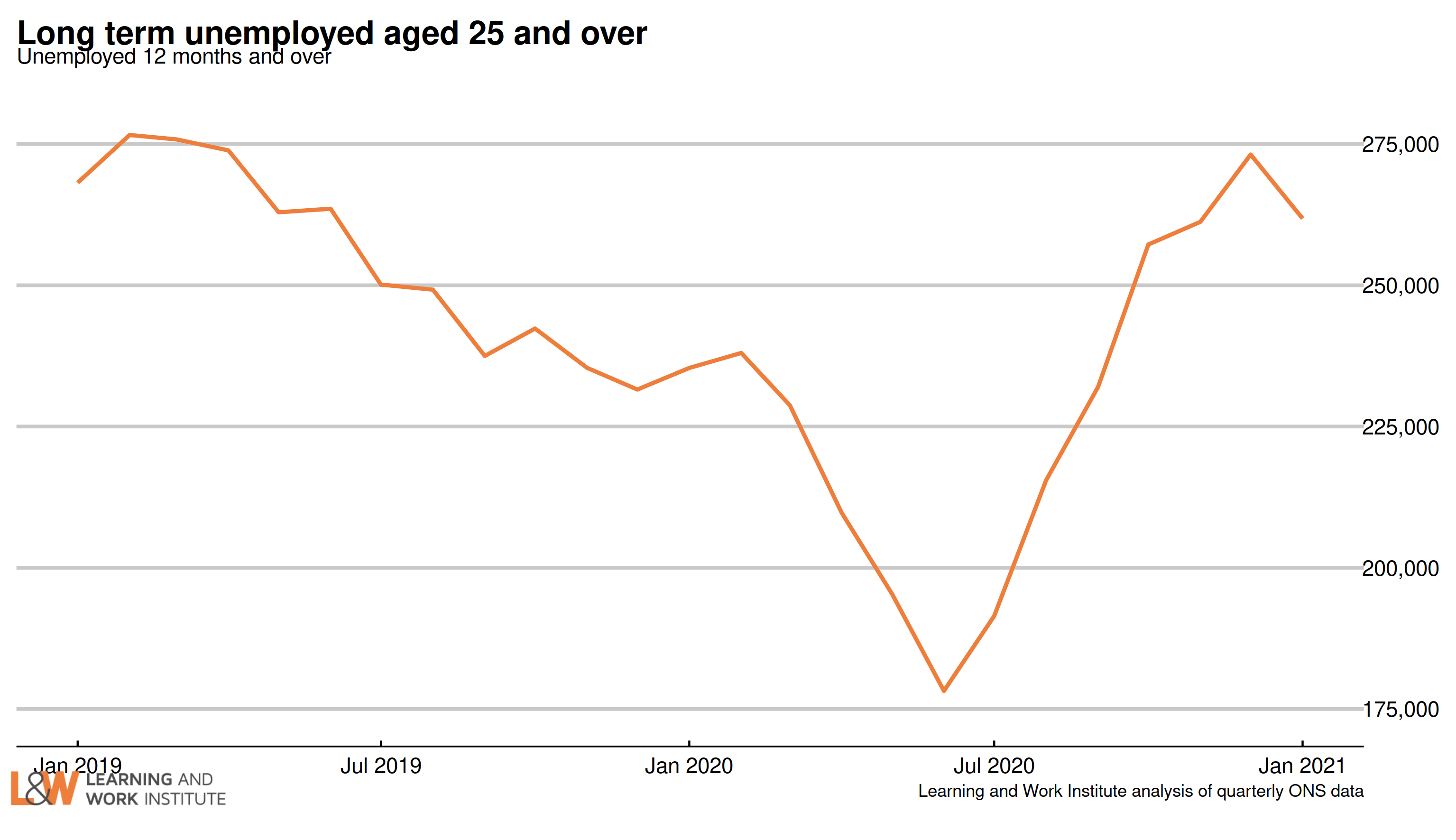

| Chart 6: Adult long-term unemployment (12 months and over, 25+) Adult long-term unemployment on the survey measure is now 262,000, up 2% on the previous quarter, and 11% on a year before. Those who lost their jobs with the first lockdown are not yet in these figures, though by now they will have passed the 12-month threshold. The fall in the first lockdown period of 2020 (April to June 2020) could be due to long-term unemployed people stopping looking for work at that time. Later, they then resumed looking for work and may have counted their unemployment from when they lost their job, missing out the lockdown period, so they came back into the figures later.  |

|

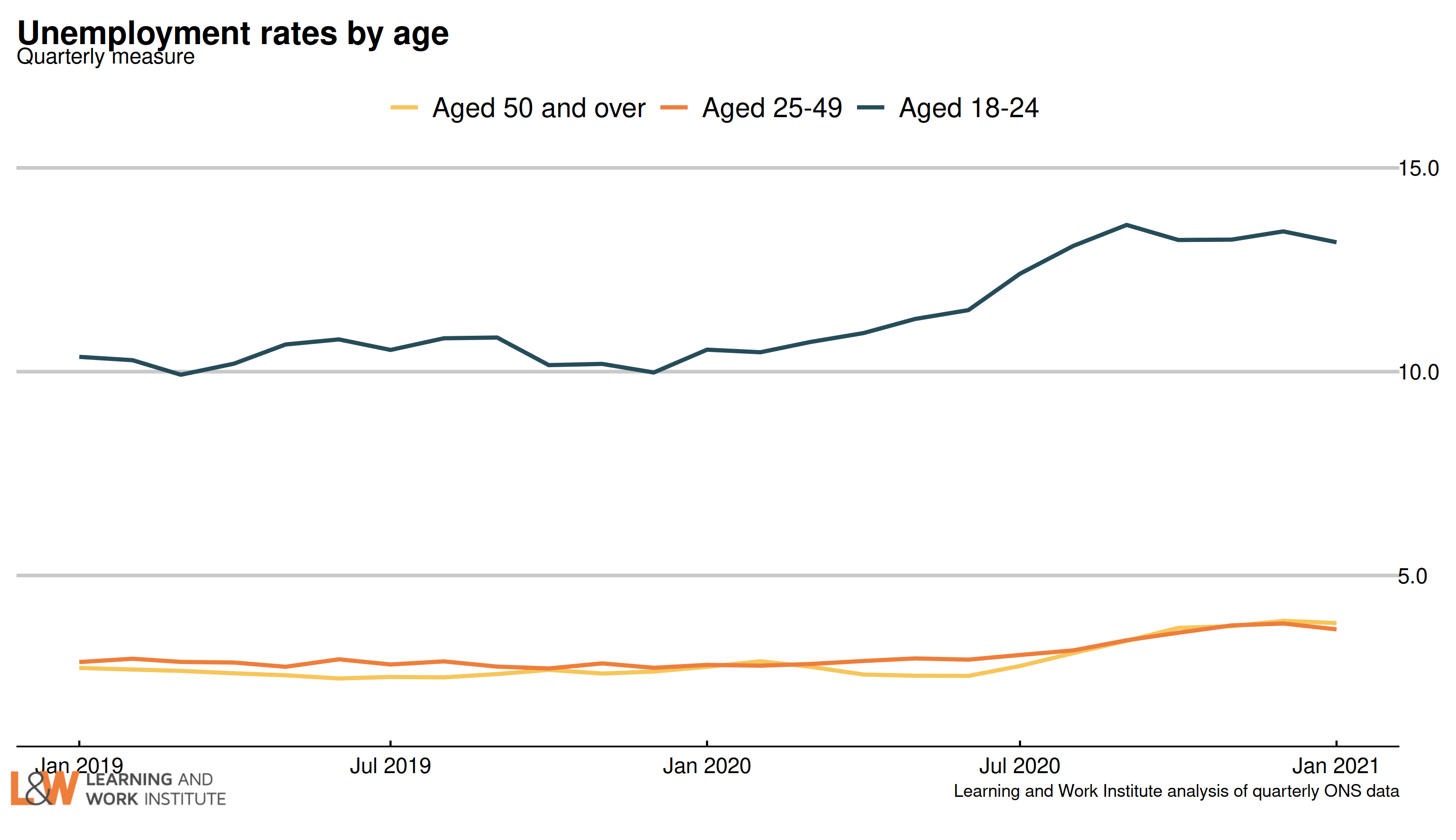

| Chart 7: Unemployment rates by age The 18 to 24 year old unemployment rate (including students) is 13.2% of the economically active – excluding over one million economically inactive students from the calculation. The rate for those aged 25 to 49 is 3.7%. For those aged 50 and over it is 3.8%. There was a fall of 0.1 percentage points for 18 to 24 year olds, and a rise of 0.1 percentage points for both 25 to 49 year olds, and the over-50s.  |

|

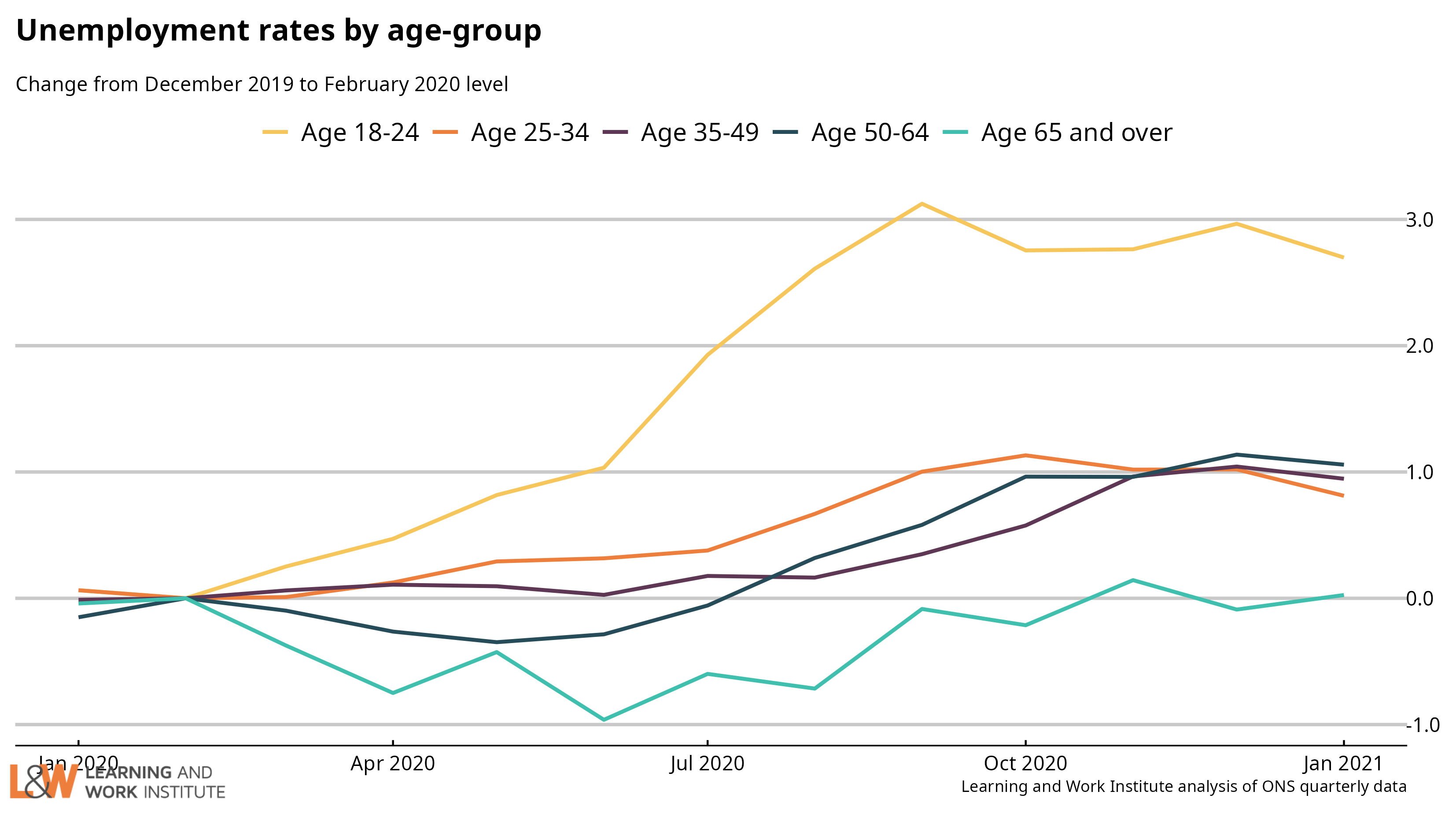

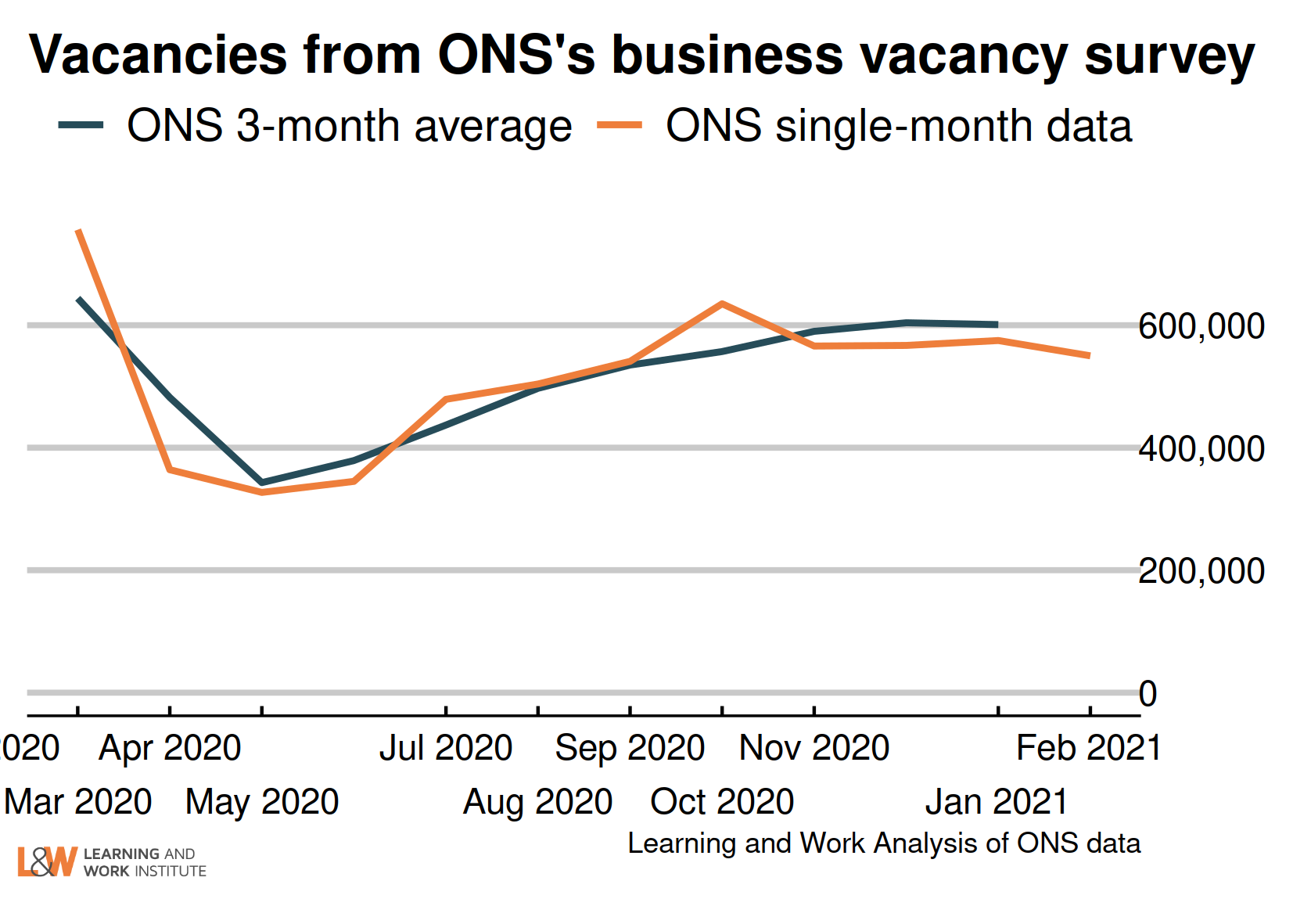

| Chart 8: Unemployment rate changes by age (counting February 2020 as 100) The 18 to 24 year old unemployment rate (including students) is 2.7 percentage points higher than in February 2020. The change for those aged 25 to 34 is 0.8. The change for those aged 35 to 49 is 0.9. The change for those aged 50 to 64 is 1.1 The change for those aged over 65 is now zero.  Chart 9: Vacancies – whole economy survey Headline vacancies this month decreased by 3,000 to 601,000. The ONS' experimental single-month vacancy figures reduced by 16,000 In the last quarter. The headline ONS vacancy figure is both seasonally adjusted and a three-month average. The chart shows both series.  |

|

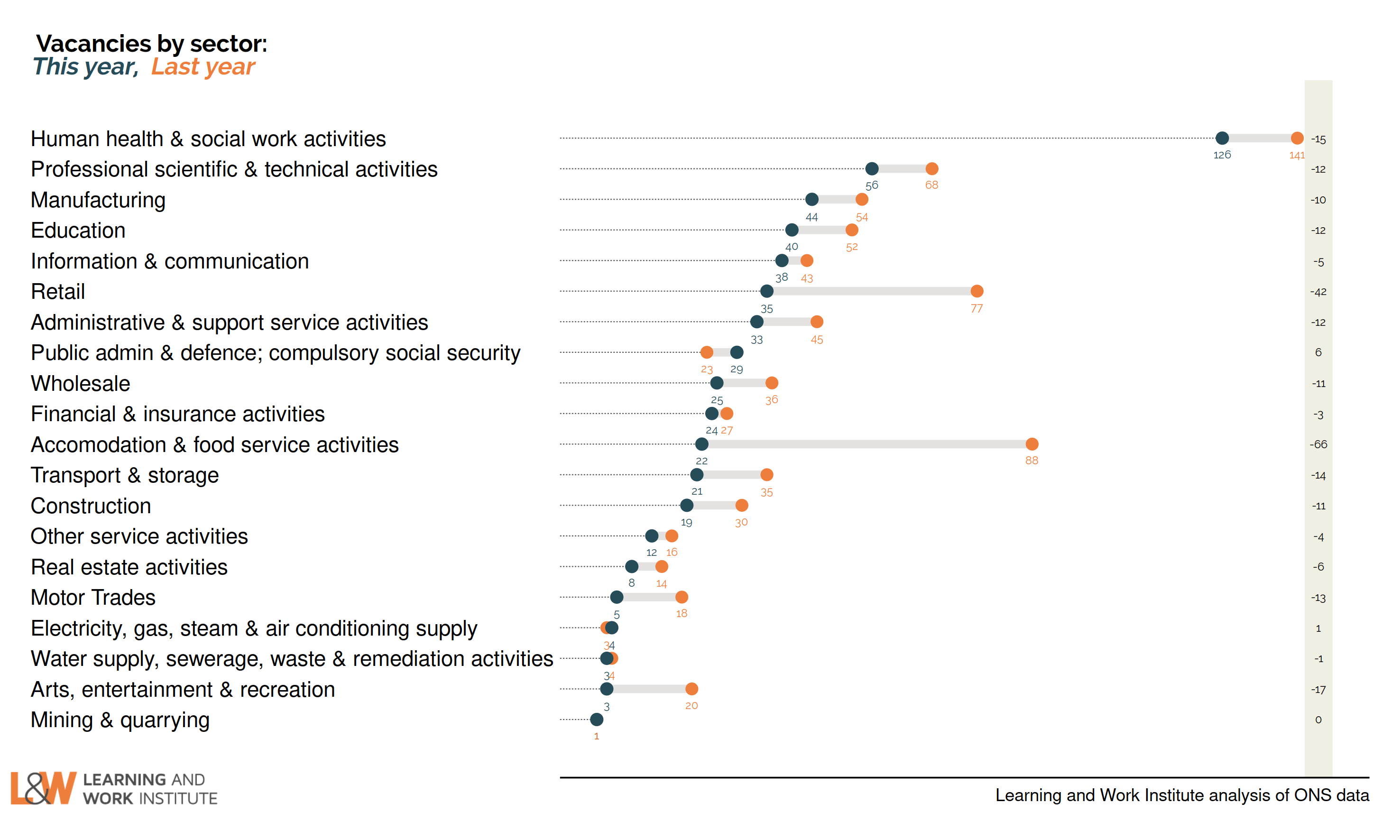

| Chart 10: Experimental single month vacancies – whole economy survey The Office for National Statistics experimental single month vacancy estimates include sectoral information. As these are not seasonally adjusted, it is better to look at annual changes. The numbers are thousands of vacancies, under each number, and on the right are the annual changes in thousands of vacancies. The annual falls in vacancies in the accommodation and food service sector and in retail are expected, but very large. They account for most of the total fall. Other sectors show small falls (except public administration and social security with a small rise). However, even with the very large falls in retail and accommodation and food service, vacancies exist and so they are still significant sectors for job catering.  |

|

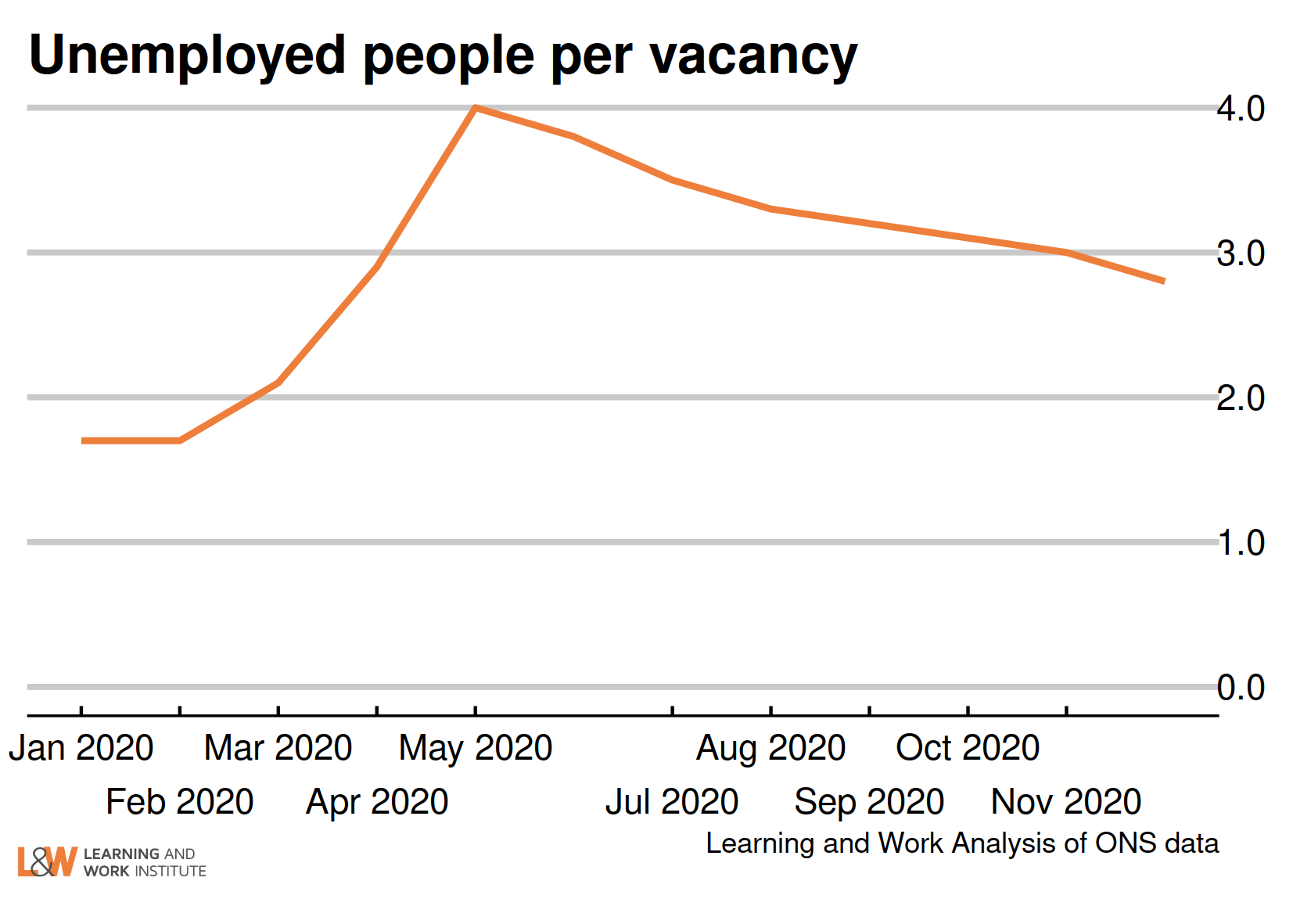

| Chart 11: Unemployed people per vacancy There are 2.8 unemployed people per vacancy. This has fallen back as the number of vacancies has risen, despite increasing numbers of unemployed.  |

|

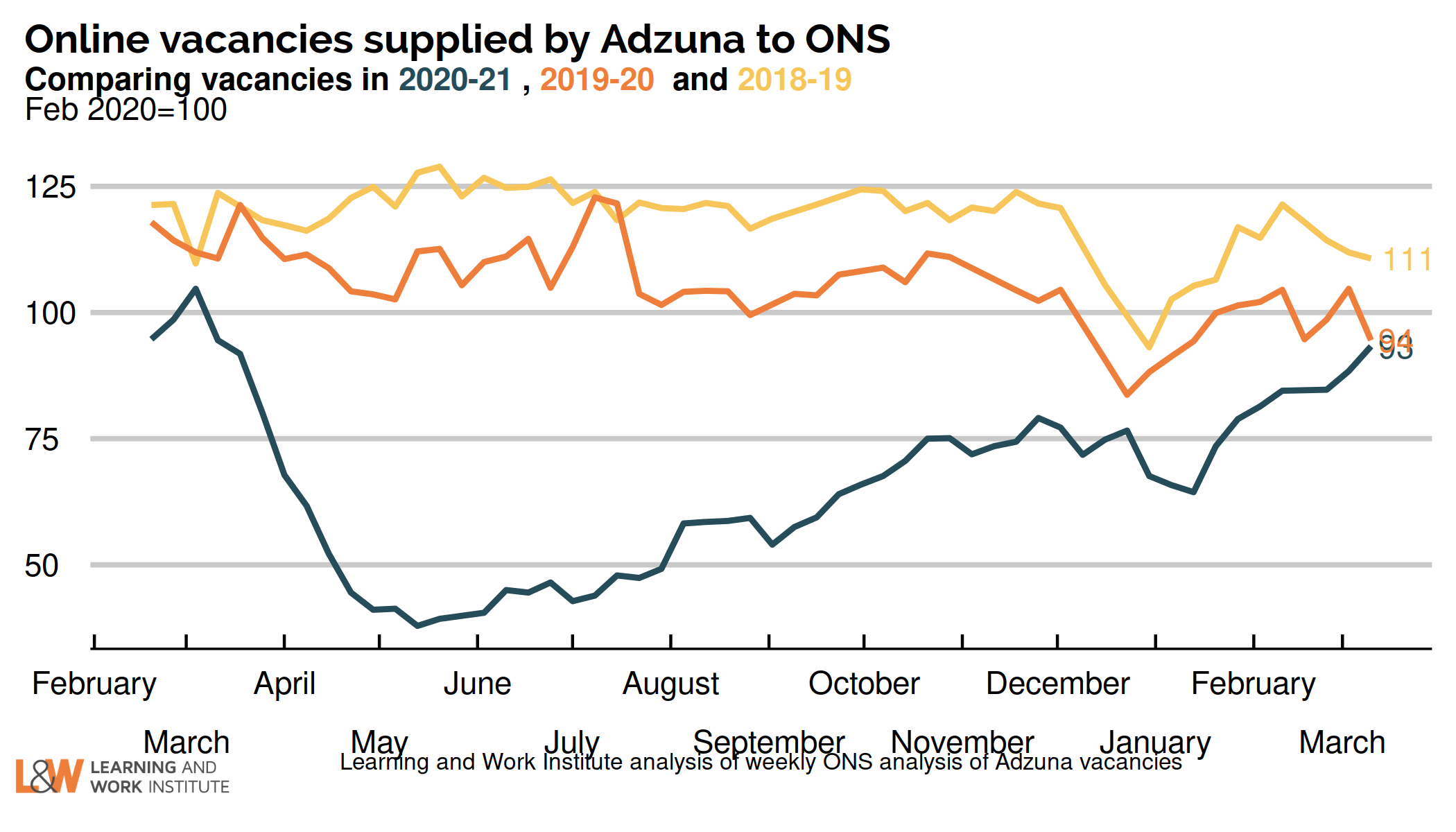

| Chart 12: Online vacancies to early March from Adzuna Job vacancies dropped to below half of the 2019 average following the first lockdown. ONS analysis suggests that it was this reduced hiring that led to falls in employment, rather than increased job loss. There had been a gradual increase as the lockdown had eased. The number of online vacancies captured by Adzuna at the start of March was 93% of February 2020 levels.  |

|

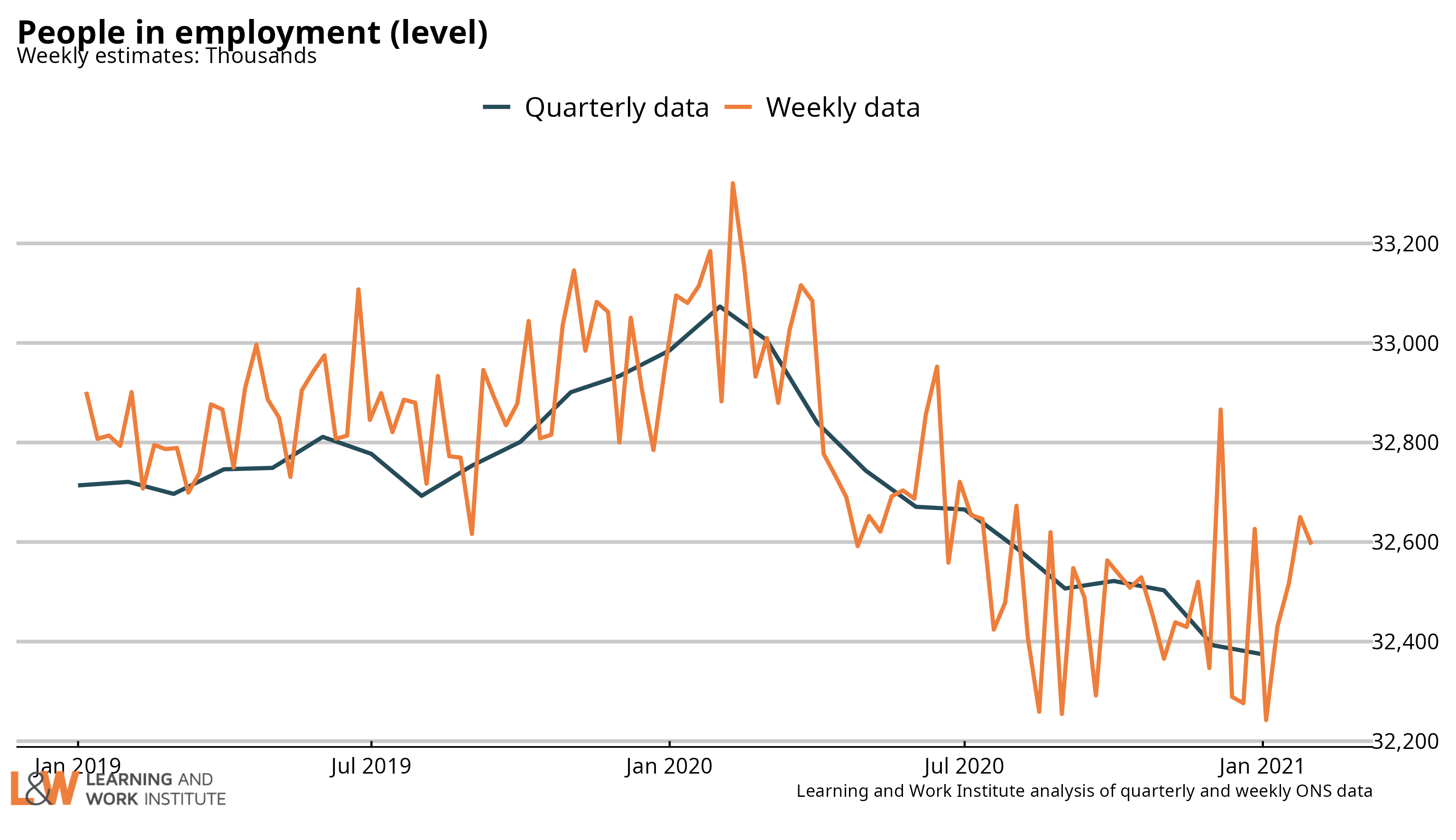

| Chart 13: UK employment Employment has fallen by 18,000 on the figure published last month, to 32,374,000. The chart shows both the official figures and the experimental weekly figures. The trend is likely to be downwards.  |

|

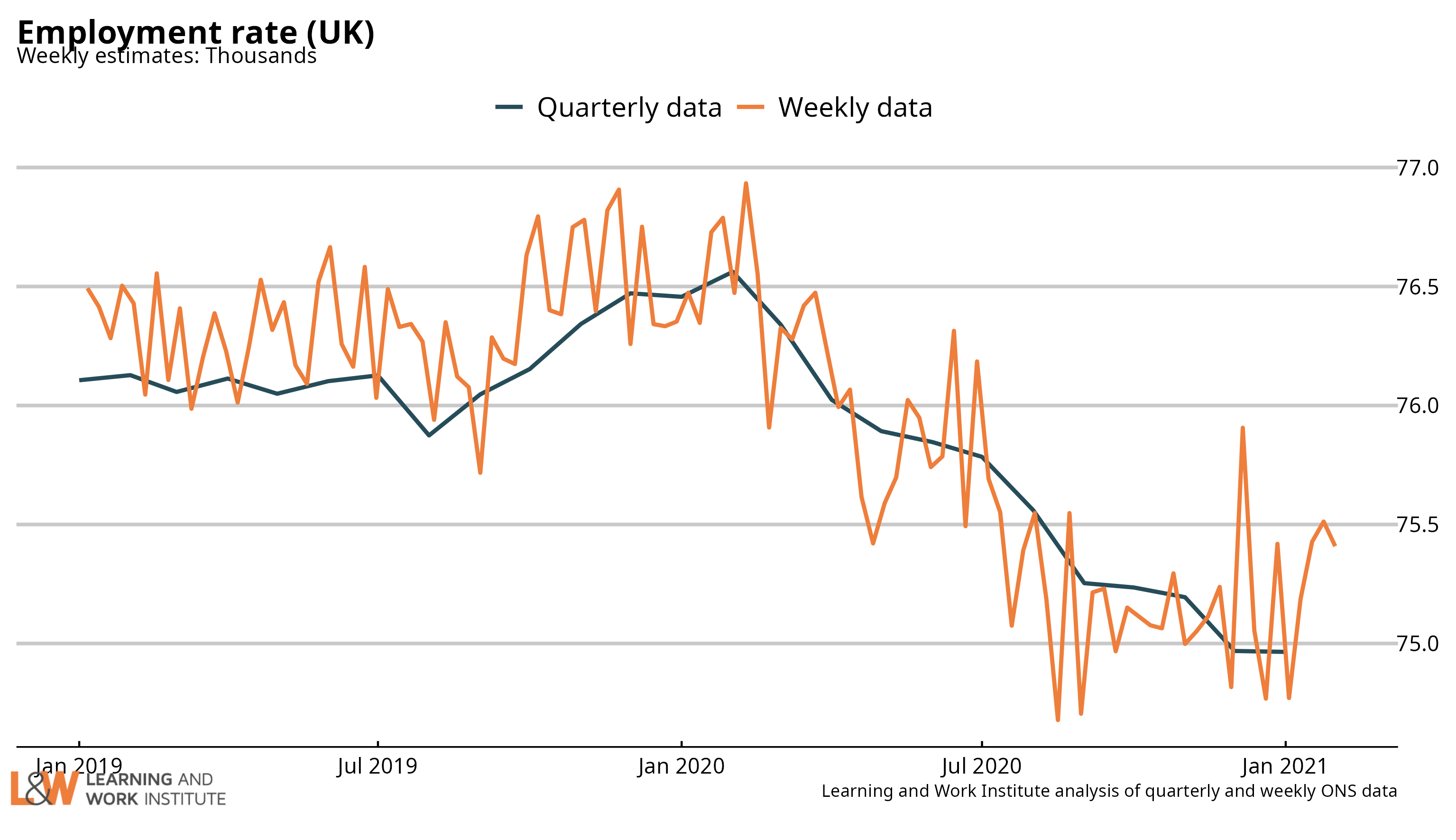

| Chart 14: Employment rate in the UK The employment rate is down by 0.3 percentage points over the quarter, to 75.0%. The chart shows both the official figures and the experimental weekly figures. The trend is likely to be downwards.  |

|

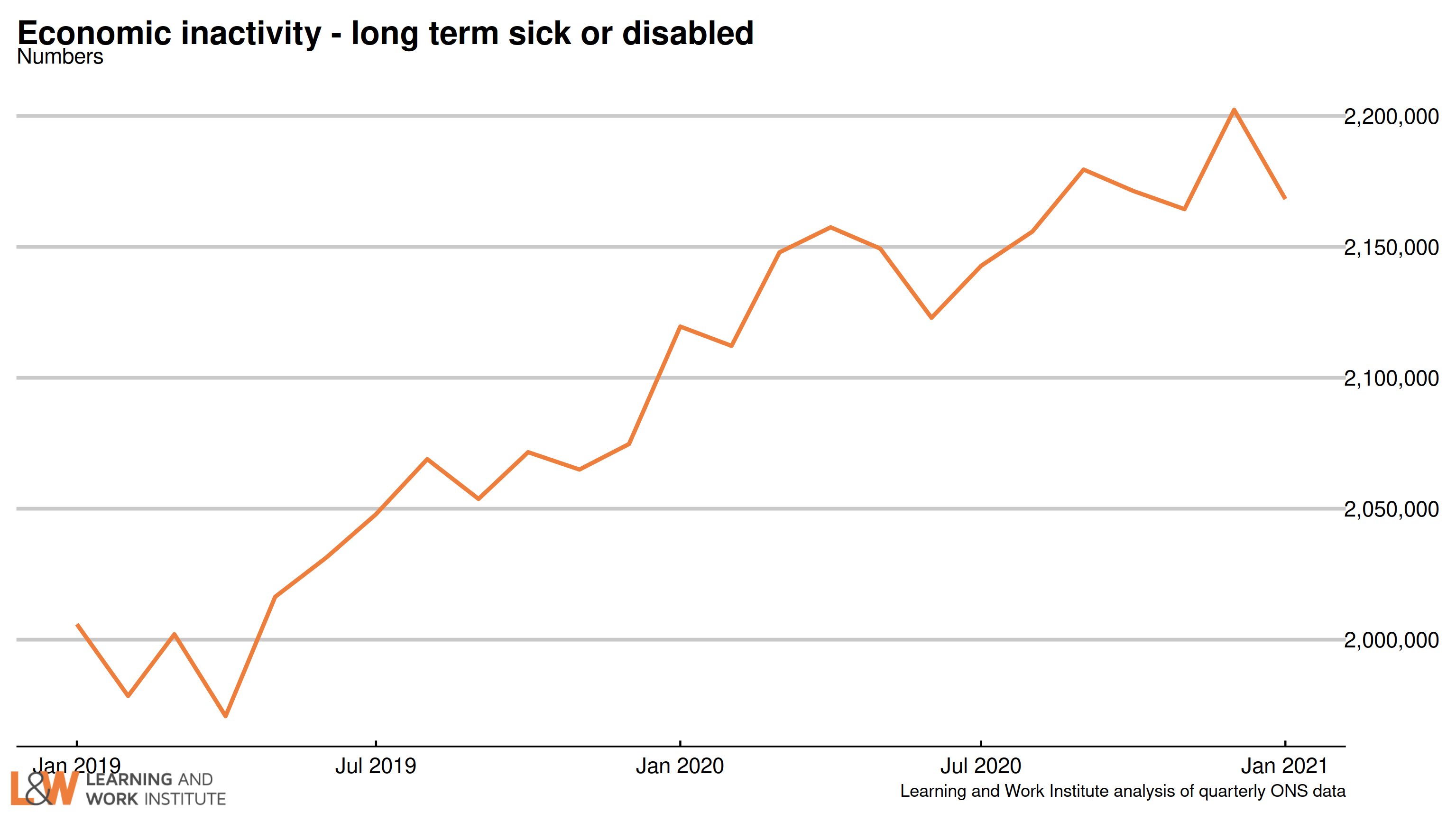

| Chart 15: Economic inactivity – the long-term sick or disabled The numbers of people who are economically inactive, that is, not working and not currently looking for work, who are long-term sick or disabled has been trending upwards. This month, we are showing the numbers of people in this group. The benefit figures are increasingly unfit for purpose due to Universal Credit statistics not identifying those who claim on health grounds. The UC statistics only identify clearly some of these (who are eligible for an additional payment).  |

|

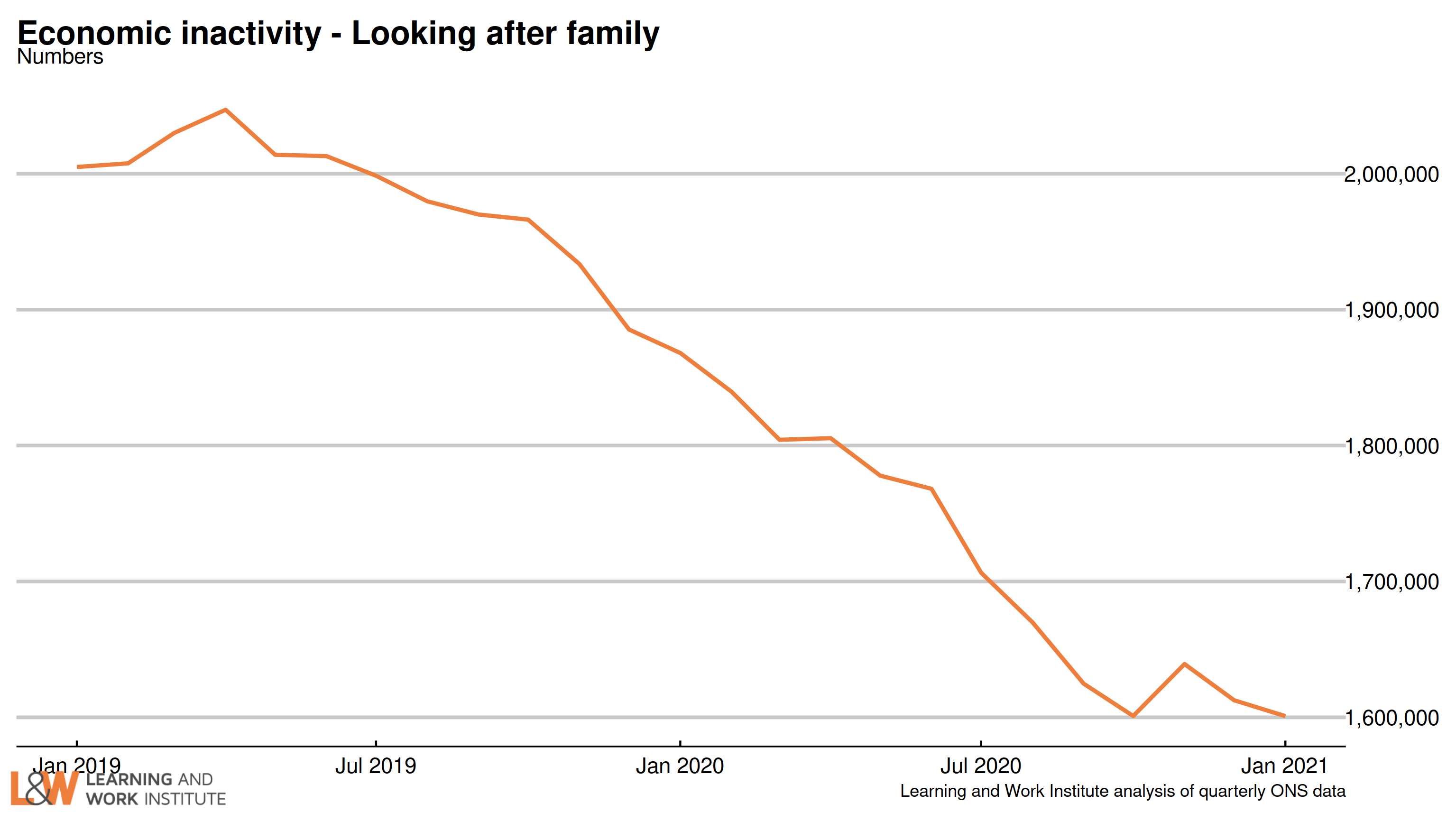

| Chart 16: Economic inactivity – people looking after family The survey figures (showing those looking after family and not doing or looking for paid work) have been trending downwards.  |

|

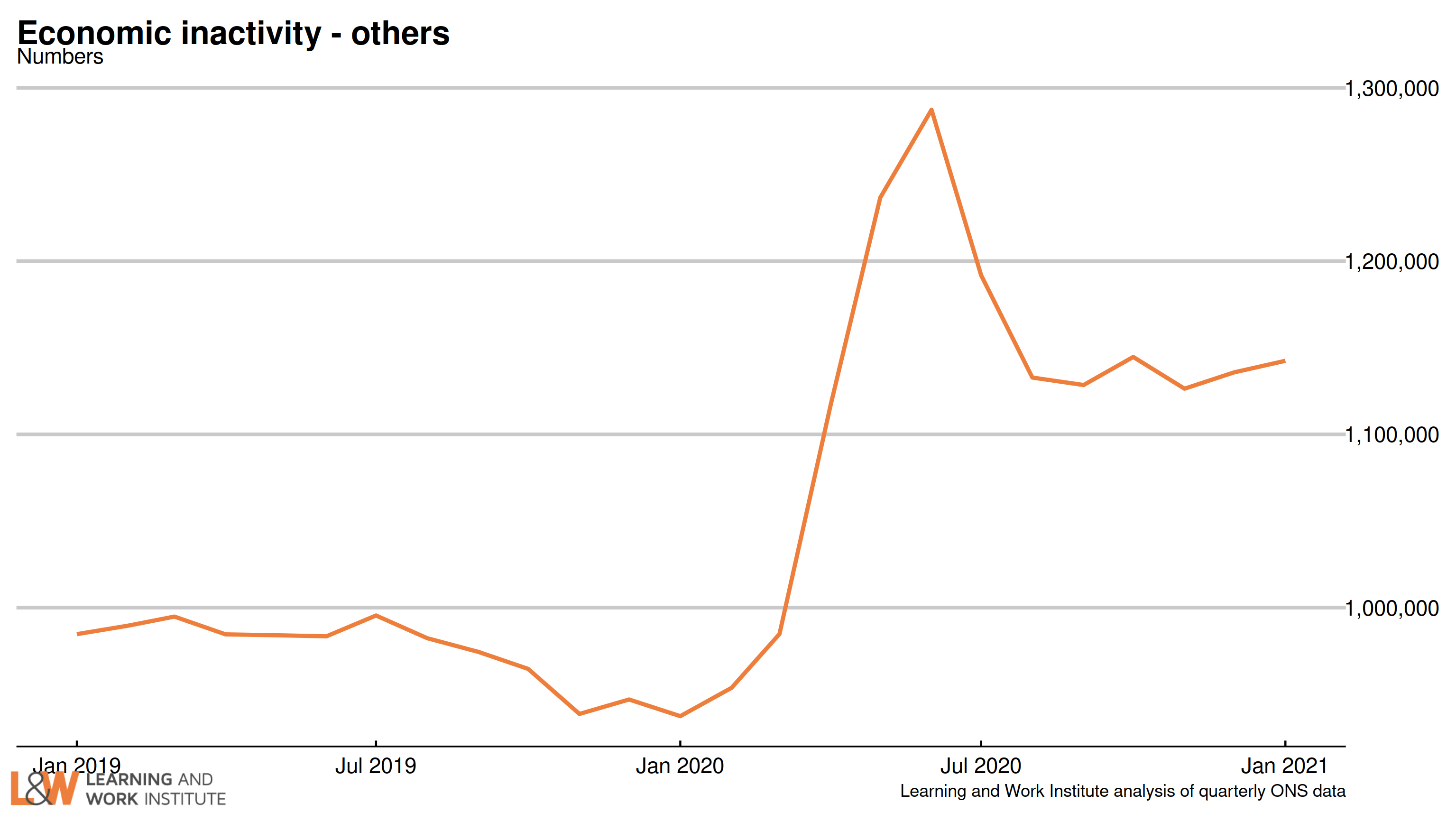

| Chart 17: Economic inactivity – other inactive In the Coronavirus period, people who were not working or looking for work due to Covid were included in this group. The number in this category increased sharply at the time, and has continued at a high level. A very high proportion of this group want to work, and this increased over the period of the pandemic.  |

|

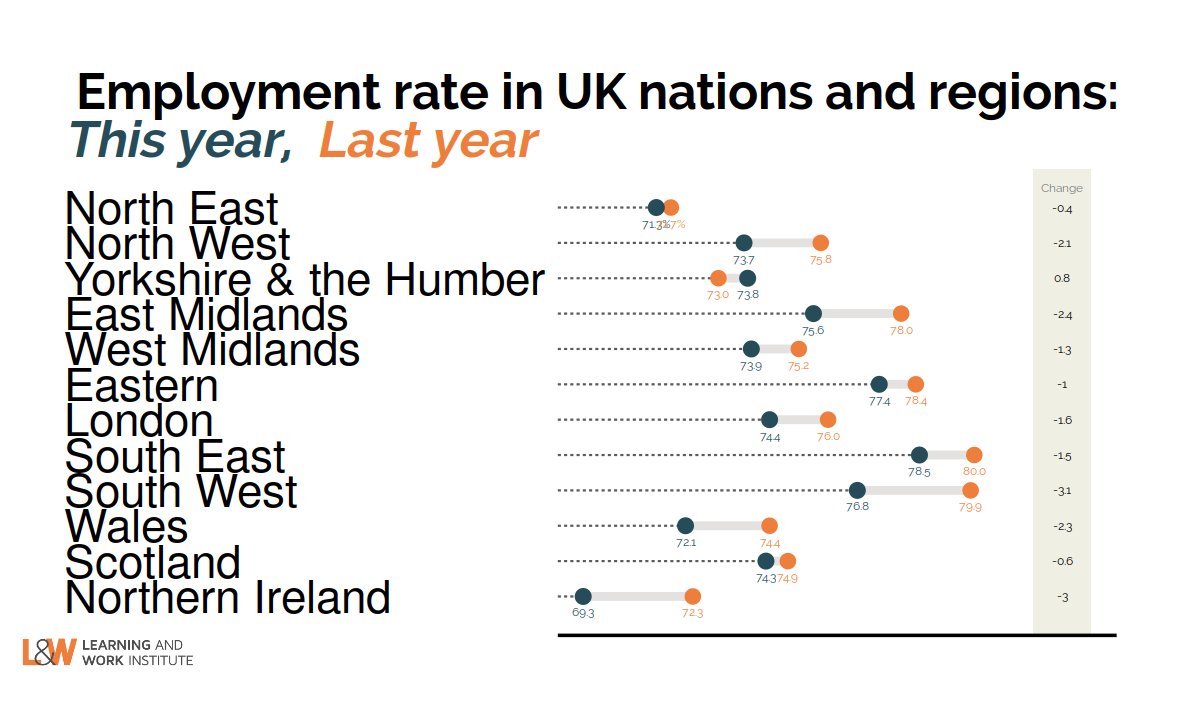

| Chart 18: Employment rate quarterly change in regions – November 2020 to January 2021 This quarter, one region showed a rise in the employment rate, Yorkshire & the Humber. The employment rate fell in 11 regions, led by the East Midlands and the South West.  |

|

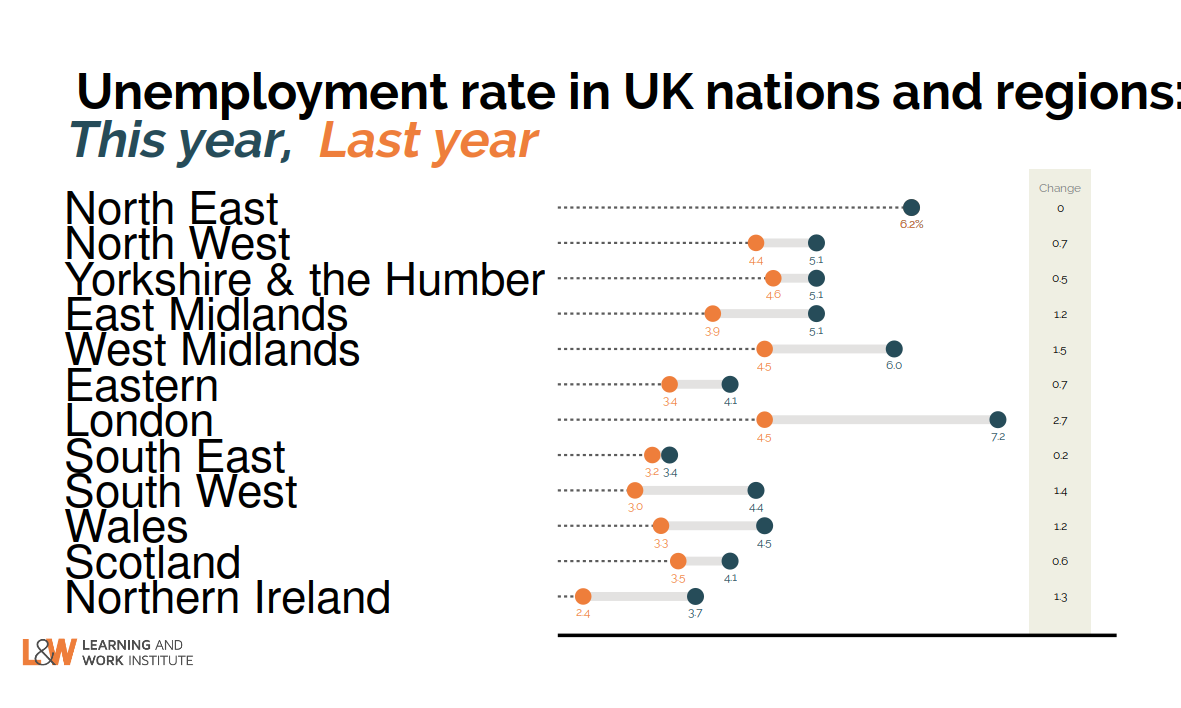

| Chart 19: Unemployment rate quarterly change in regions – November 2020 to January 2021 This quarter, 11 regions showed a rise in the unemployment rate, led by London and the West Midlands. The unemployment rate shoed no change in the North East.  |

|

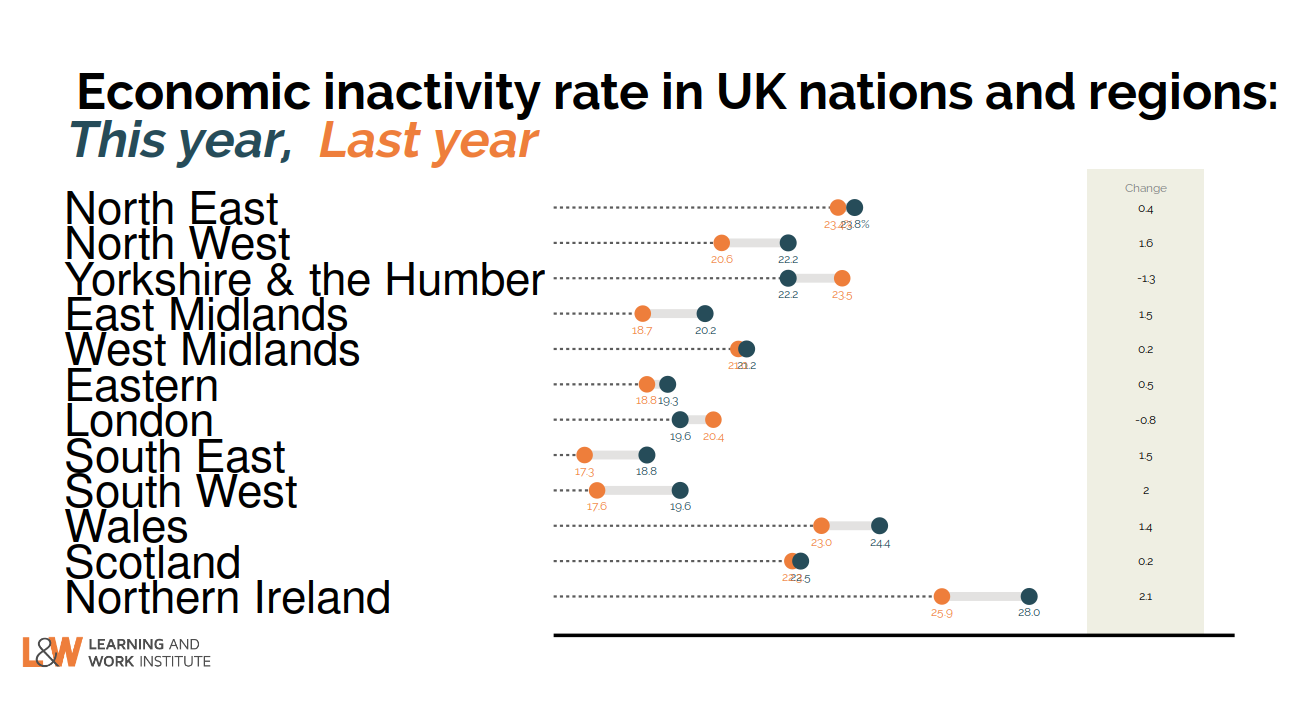

| Chart 20: Inactivity rate quarterly change in regions – November 2020 to January 2021 This quarter, 10 regions showed a rise in the inactivity rate, led by the North West and Northern Ireland. The inactivity rate fell in two regions, Yorkshire and the Humber and London.  |

|

|

This newsletter is produced by Learning and Work Institute and keeps readers up to date on a wide range of learning and work issues. |

|